US Dollar Index bounces off 2-month lows near 90.40 ahead of data

- DXY regains some composure following multi-week lows.

- US 10-year yields edge higher and approach the 1.65% area.

- Flash Q1 GDP figures, weekly Claims, housing data next on the docket.

The greenback manages to regain the smile and bounce off earlier 2-month lows near 90.40 when tracked by the US Dollar Index (DXY) on Thursday.

US Dollar Index depressed post-Fed, looks to data

The index remains largely on the defensive so far this month, losing ground for the fourth consecutive week so far and about to close the first month with losses after three consecutive monthly advances.

The dovish tone from the FOMC event on Wednesday exacerbated the selling bias surrounding the buck, particularly after Chairman Powell once again ruled out any modification of the Fed’s forward guidance and/or the bond-purchase programme in the foreseeable future, all despite positively assessing the pace of the US economic recovery.

In the meantime, investors continue to favour the risk complex and keep looking to the progress of the vaccine rollout and the economic recovery outside the US, all collaborating with the persevering bearish sentiment in the dollar.

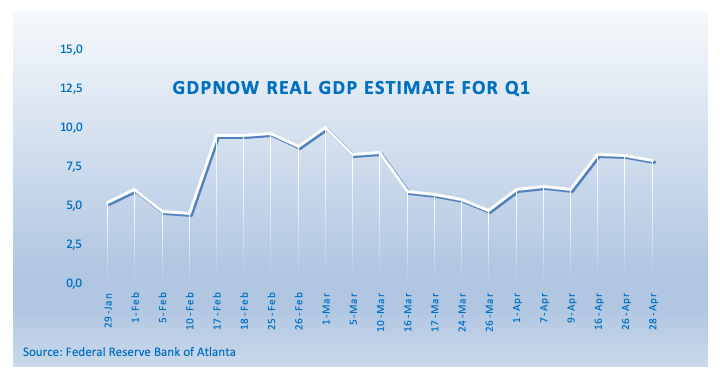

Later in the US calendar, the focus of attention will be on the flash Q1 GDP figures seconded by the usual weekly Claims and Pending Home Sales.

What to look for around USD

The April pullback in the dollar remains well and sound despite the ongoing rebound from 2-month lows in the 90.40 region. The move lower in the buck follows the broad-based retracement in US yields and the loss of enthusiasm on the US reflation/vaccine trade. Also weighing on the dollar emerges the mega-accommodative stance from the Fed (until “substantial further progress” in inflation and employment is made), and rising optimism on a strong global economic recovery, all morphing into a solid source of support for the riskier assets and a most likely driver of probable weakness in the dollar in the next months.

Key events in the US this week: Flash Q1 GDP, Initial Claims (Thursday) – Core PCE, Personal Income/Spending, final April U-Mich Index.

Eminent issues on the back boiler: Biden’s new infrastructure bill worth around $3 trillion. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating?

US Dollar Index relevant levels

Now, the index is gaining 0.07% at 90.65 and faces the next support at 90.42 (monthly low Apr.29) followed by 89.68 (monthly low Feb.25) and then 89.20 (2021 low Jan.6). On the other hand, a breakout of 91.42 (high Apr.21) would open the door to 91.66 (50-day SMA) and finally 91.99 (200-day SMA).